These documents contain excerpts about property prices in Malta, mdina and valletta obtained from the Central Bank Annual Reports issued between 1998 and 2009. Excerpts taken from the Central Bank Annual Reports:

http://www.centralbankmalta.com/site/publications2.asp

To view a particular document click on one of the 'View Report' links below. You are also

able to download the respective documents by right-clicking on one of the 'Download Report' links and selecting 'Save Target As...'

The slowdown in the rate of increase in property prices

observed in 2005 continued throughout 2006,

particularly in the latter half of the year. Advertised

property prices rose by 3.7%, significantly less than

the 10.4% recorded in 2005 (see Chart 3.3).

This slowdown in house price inflation reflects a

deceleration across most property types, particularly

terraced houses, maisonettes and finished flats, the

latter accounting for over 40% of sampled properties.

In contrast, asking prices for town houses rose by

2.3%, after having declined in the previous year, while

prices of flats in shell form and villas rose at a faster

pace than in 2005.

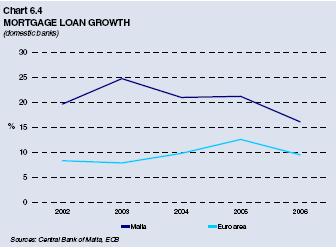

Household indebtedness to banks continued to

increase during 2006, with the rate of growth of

mortgage lending in Malta remaining higher than the

euro area average (see Chart 6.4).8 However, although

households remained vulnerable to shocks, the debt

burden still appears to be sustainable. Indeed, while

rising interest rates impinged on their debt repayment

capability, this negative effect was offset by the

positive influences of higher employment levels and

growth in national income. Affordability has also

improved, while problematic loans have decreased

further.9 Furthermore, households are still

accumulating wealth, both financial and propertyrelated,

thus indicating an increasing buffer to service

debt.

Nevertheless, although the financial position of

households remains sound, and even appears to have

strengthened during 2006, an acceleration in the debt

burden poses some risks going forward. Since most

mortgage loans are contracted at variable rates,

households with a heavy debt burden, particularly

those in the lower income bracket, become more

vulnerable in an increasing interest rate scenario.

.: SIMON Estates (Naxxar) Ltd :.

159, Il-Gebla, Labour Avenue, Naxxar. Malta

223, Republic Street, Valletta. Malta

6, Chemin du Repos, 1213 Petit-Lancy, Geneva, Switzerland

Tel: 00356 23 88 00 10

Mob: 00356 79 00 82 87